Tuesday 27th May 2025

The case against complacency: Why the S&P/ASX 200 is holding advisers back

Dion Hershan, head of Australian equities at Yarra Capital Management, doesn’t believe in sugar-coating market narratives. His message to The Inside Network’s recent Equities and Growth Symposium was that the main Australian sharemarket index was "broken."

At the recent Equities & Growth Symposium, Yarra Capital’s Dion Hershan took direct aim at what he calls “the old favourites” of Australian equities — banks, miners, and the comfortable top 20 — and offered a brisk, data-driven case for breaking away from the benchmark. Hershan’s call wasn’t just a pitch for mid-cap stocks; it was a call to arms against complacency, a challenge to entrenched allocation habits, and a roadmap for future-proofing portfolios in a rapidly evolving economic landscape.

Hershan opened with a stark reminder of how entrenched legacy positioning has become. Most Australian investors, he said, still allocate the lion’s share of their equities exposure — either passively or through low-tracking-error funds — to the S&P/ASX 200. That would be fine, he argued, if the index were well-balanced and forward-looking. But it’s not. “If you were building a portfolio from scratch, you’d never pick this,” he said. “You’d never want 40 per cent of your capital tied up in four banks and one commodity.”

The numbers back him up. Over the last eight years, the earnings of Australia’s big banks have been flat or declining. Margins, once the envy of the world, have been in secular decline since the birth of the mortgage broker industry in the 1990s. Return on equity for the big four has dropped from over 20 per cent to around 11 per cent, while the sector’s exposure to rising costs and stagnant mortgage growth compounds the problem. Despite a rally in 2024, Hershan described the sector’s prospects bluntly: “No growth. No cost control. And valuations that are wildly optimistic.”

The outlook isn’t much better for the miners. Hershan cited China’s steel industry — responsible for 71 per cent of global seaborne iron ore demand — as being effectively flat for the last five years. With China’s property sector maturing and massive amounts of new supply from Guinea’s Simandou project set to come online, he believes the iron ore market is heading toward oversupply. A seemingly modest price fall from US$100 to US$80 a tonne could slash BHP and Rio’s earnings by 40 per cent. “These are not diversified miners,” he stressed. “They’re iron ore businesses in disguise.”

Perhaps most damning is Hershan’s analysis of organic growth. Among the S&P/ASX 20, not a single company is forecast to grow revenue by more than 10 per cent annually. Compare that to the Ex-20, where 24 per cent of constituents are achieving that level of growth. The data is consistent across timeframes: over the past decade, the Ex-20 has outperformed both large-caps and small-caps, with lower volatility. Yet institutional portfolios remain overweight the top 20, largely out of habit. “Everyone knows the risks,” Hershan said. “Very few people are doing anything about them.”

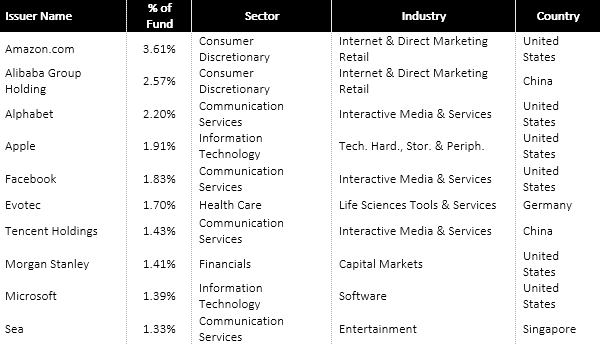

That inertia, he argued, is costing investors both performance and diversification. The Ex-20 offers broader sectoral exposure — tech, new media, and battery minerals are all under-represented in the S&P/ASX 20 — and higher active share. It’s not a dumping ground for second-tier stocks, it’s where Australia’s next global champions are emerging. Companies like ResMed, Xero, and Carsales, all of which combine global ambition with proven operating leverage, are thriving outside the benchmark spotlight. “CSL’s growth has stalled. ResMed’s is accelerating. But CSL still gets the flows,” he said. “Why?”

Even on a value basis, the Ex-20 stacks up. Hershan highlighted examples like Block (formerly Afterpay), trading at a discount to the banks despite growing earnings at more than 25 per cent annually. Elsewhere, companies like QBE, APA Group, and Ansell offer stable yields and global earnings streams — exactly the characteristics advisers seek in core holdings, but too often overlook due to their benchmark positioning. “We think this is lower-risk, not higher,” he said. “You’re not over-exposed to one commodity or one sector. You have choice.”

He’s also realistic about the comparison to small-caps. While small-caps can offer outsized returns, they’re often plagued by illiquidity, unproven business models, and a high rate of loss-making miners. In contrast, Hershan described the Ex-20 as the “sweet spot” — a $1 trillion investible universe, with twice the liquidity of small-caps and a broader set of sector exposures. “In a typical small-cap index, 40 per cent of mining companies don’t produce anything,” he said. “In the Ex-20, 100 per cent of mining stocks are producers.”

What struck a chord most was Hershan’s clarity on risk. While many view a benchmark-tracking portfolio as a safe option, he sees the opposite. The S&P/ASX 20 is heavily concentrated, highly correlated, and anchored to legacy industries with dim growth prospects. Passive investing, he warned, is effectively momentum investing — buying big companies just because they’re big, not because they’re better. “In the US, that’s worked, because the biggest companies have delivered. In Australia, it’s more often size without substance.”

As he wrapped up, Hershan reiterated the structural advantages of the Ex-20: growth, diversification, and the opportunity for alpha. But more than that, he made a broader appeal for intellectual honesty. Advisers, he argued, need to question the logic of continuing with asset allocations that are demonstrably outdated. “It’s a comfortable place to be, but that doesn’t make it the right place to be,” he said. In an uncertain economic environment where old correlations are breaking down and new industries are scaling up, the safest move might be the one that feels the least familiar.

James is an experienced senior journalist and editor of The Inside Network's publications.