Thursday 5th June 2025

Once in a decade: The return of real value

Reece Birtles doesn’t see value investing as a relic. Far from it. The chief investment officer at Martin Currie Australia believes the strategy is not only relevant in today’s market — it’s poised for a resurgence.

Speaking at The Inside Network’s 2025 Equities and Growth Symposium, Martin Currie’s Birtles laid out a compelling case for a shift already underway: the return of fundamentals, the re-emergence of pricing discipline, and a new opportunity set that he calls “the best in decades.”

For Birtles, the message is clear: active management is back, value is back, and the environment has fundamentally changed. Not in some technical, interest-rate-tinkering sense, but structurally. “All of those traditional factors — valuation, quality, earnings revisions — they only work when money costs something,” he said, plainly. For the past two decades, they didn’t. With bond yields suppressed and equity correlations flipped, value managers were left fishing in shallow, murky water. But now? “The excess annual return from valuation strategies is back at 7 per cent. That hasn’t happened since before 2000.”

This is not value as caricature. Birtles is quick to distance himself from the clumsy framing that paints value investing as inherently anti-growth, or worse, anti-quality. “We’re not buying low price-to-book stocks for the sake of it,” he said. “We’re buying discounted cash flow streams. And we care about quality. We care about growth.” His team’s approach is multi-pronged — valuation, quality, momentum — and their edge is not dogma but discipline. “It’s a weighing game. The more contrary the idea, the greater the potential return must be.” In other words, being right isn’t enough. You have to be early, and you have to survive long enough for the market to catch up.

Survival isn’t always a given. There are scars here, too. Birtles cites G8 Education as a lesson in how cheap stocks can stay cheap, or worse. “We were looking for occupancy improvements. Then COVID hit. Suddenly there’s a rights issue and the value’s destroyed.” But the counter-balance — the redemptive, affirming trade — is JB Hi-Fi, a long-term holding he first bought in 2011 when the market had all but written it off. “Amazon was coming. It was trading under 10 times earnings. But we saw it as the best retailer in the country. Everyone was wrong.” JB Hi-Fi went on to become a darling, but for Birtles, the real win wasn’t in the rerating: it was in seeing clearly when others couldn’t.

Seeing clearly is a kind of rebellion in today’s market. In Birtles’ view, prices no longer reflect information; they reflect flows. “The price of Commonwealth Bank isn’t where it is because of fundamentals. It’s there because it’s in the index.” Passive flows, he explains, are distorting markets more aggressively than most care to admit. “At 11am, the index-aware super fund comes in and buys the stock at yesterday’s price. It doesn’t matter if it’s over-valued. They’re not looking for price discovery. They’re just deploying capital.” It’s not just passive funds, he adds. It’s the entire index-aware ecosystem that has made fair value an afterthought.

This distortion is now measurable. Birtles’ team tracks the percentage of daily turnover attributable to index flows — a figure that’s risen sharply post-COVID. Liquidity is evaporating in the largest stocks, while their prices drift further from intrinsic value. “CBA’s daily volume has collapsed, and yet the price keeps going up. Then earnings season hits, new information arrives, and bang — the price gaps 10 per cent in two days.” This isn’t volatility; it’s malfunction. And to Birtles, it’s an opportunity. When the machine breaks, the humans win.

Australia, it turns out, is the perfect theatre for this battle. Compared to global equity markets, the ASX is structurally inefficient. “In global portfolios, there’s too much macro noise. You’re overweight European banks, underweight US tech, and it’s impossible to separate the signal from the noise.” But in Australia, the macro is more consistent. Regulatory frameworks are clearer. That means fewer variables, better decisions, and — crucially — more alpha.

And there’s more. The median Australian equity manager, according to Birtles, delivers more alpha than their global counterparts. It’s not because they’re smarter: it’s because the market lets them be. “We can position one bank versus another. We can position against resources. The decisions are cleaner.” But the risks are systemic. He’s deeply concerned about the concentration of ownership among APRA-regulated super funds. “They own 35 per cent of the equity market, 35 per cent of the debt market. That’s a structural risk, and one we don’t talk about enough.”

Amid the noise, Birtles keeps refining his edge. His team disaggregates factor exposures — momentum, beta, size — to isolate what he calls “pure alpha.” Not style rotation, not cyclical tailwinds, just the decisions analysts make, measured against clean benchmarks. “You can look at a fund’s style ‘skyline’ and think they’re outperforming. But most of the time, they’re just on the right side of a momentum cycle. That’s not skill.” For large clients, Martin Currie even builds style-neutral portfolios, stripping-out the factor biases completely. “It means the index flow effect doesn’t impact you. You’re just matching one distorted stock against another.”

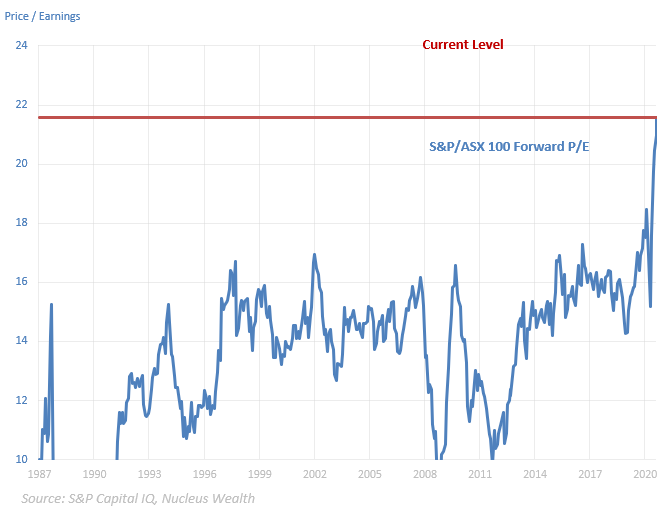

So, what does he see today? A once-in-a-decade setup. His internal models show a 40 per cent discount to fair value in the current portfolio — double the long-term average. “That’s a 15 to 20 per cent alpha opportunity. We saw it after the tech crash, after the GFC, during COVID. But now? It’s happening again.” The only difference, he notes, is that the stocks are better. “These aren’t high-beta, distressed names. They’re high-quality, low-risk. They just haven’t kept up with the hype.”

If that sounds like déjà vu, it’s because it is. “Our portfolio today looks like it would have looked in 2000. Not in the holdings — but in the risk-reward profile. High-quality, undervalued, ignored.” And yet, he doesn’t sound triumphant. He sounds vigilant. Markets don’t stay mispriced forever. You need to be early — but not so early that you get crushed waiting.

When asked about future threats, Birtles doesn’t reach for AI or geopolitics. He reaches for Salesforce. “Australian companies outsource their IT to a US provider, it’s cheap on day one, and then the price goes up 15 per cent a year. After five years, you’re paying way more and you’re locked-in.” It’s an old-school gripe. But it cuts through the hype: short-term innovation often becomes long-term rent extraction.

It’s a strange thing, watching a value manager talk like a revolutionary. But Birtles’ revolution is quiet, data-backed, and rooted in a deep belief in fundamentals. He doesn’t want to be right in theory. He wants to own the olive farm, press the oil, bottle it and sell it — as he does when he’s not working. He wants to be early, yes — but also tangible. In a market increasingly dominated by flows, algorithms, and apathy, that’s as radical as it gets.

James is an experienced senior journalist and editor of The Inside Network's publications.