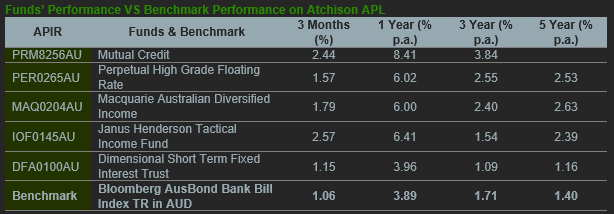

Sunday 15th December 2024

Lower mid-market ripens for agile private equity purveyors

What the Brisbane-based lower-mid tier private equity group is pulling off is emblematic of the success private equity players are enjoying in recent times. But each PE player has their own unique strategy that largely defines just how well they're doing.

While the remarkable growth of private credit has gobbled up managed investment headlines in the past few years, the other pillar of private markets – equity – continues to produce innovation and a level of robust dynamism.

Part of what’s driving this surge in private equity is the recent generation of providers who are finding their own niche and thriving in new and inventive ways. For Brisbane-based PE purveyors Fortitude Investment Partners, the cornerstone of that niche is the specific market they target.

Fortitude, which just announced a gross IRR of 30 per cent for 2024 and a total net capital return of $625 million for investors, operates specifically in the lower to mid-tier, investing $10 million to $50 million into companies with an enterprise value between $10 million and $150 million within a genuine partnership structure. They then typically, but not always, offload to larger equity players once they’ve helped a company build scale and profitability.

“There’s riches in niches,” co-founder Nick Miller told The Inside Adviser earlier this year.

Fortitude operate a small, but very specific spoke of the private equity wheel, and their strategy is idiosyncratic in a number of other ways. The partnership structure they’ve adopted, for example, is more than just lip service to co-operative relationships. Fortitude has around 130 “operating partners”, who are in fact a tight-knit network of industry experts that specialise in the handful of sectors and geographies Fortitude invests in.

They also only focus on a handful of sectors – healthcare, technology, food and industrial (particularly related to the energy transition) – and limit their investee companies to those that can demonstrate a competitive advantage and a robust growth pipeline.

But their adopted strategy is one that has seen them pull off a high number of impressive company exits in recent times. This year, for example, the group sold its holding in food product provider Birch & Waite to another private equity outfit, Quadrant.

“The Birch & Waite transaction underscores our commitment to delivering exceptional outcomes for our investors,” Miller said.

“Private equity investments allow us to take a hands-on approach, optimising operational performance and strategically positioning businesses for growth,” Miller continued. “This adaptability and focus on tangible value creation provides investors with a reliable pathway to generate strong returns over time.”

As investors from all pools of capital further warm to alternatives in the private capital arena, Miller believes the pipeline will remain strong for private equity providers.

“We expect institutional and high-net-worth investors to favour capital allocation to private equity, drawn by its proven track record of resilience and growth across market cycles,” he said.