Monday 16th March 2026

Conflict worsens the picture for levered credit

Leveraging an investment-grade credit portfolio was already a dubious strategy before the Middle East war broke out. It's now an even worse idea, says Yarra Capital Management.

As credit spreads normalised through 2025, and in some segments moved below long-term averages, yield‑hungry investors turned to leverage to maintain 6 per cent-plus returns.

But as always with leverage, investors need to be careful to understand the true risk-return trade-off. “The use of leverage to enhance returns can work very effectively in environments of stable or contracting credit spreads,” says Phil Strano, head of Australian credit research at Yarra Capital Management. “It is a double-edged sword, however, with the combination of widening credit spreads and leverage usually resulting in significant drawdowns.”

And with the war in the Middle East sending the oil price surging, and presaging economic turmoil through supply-chain disruptions in a range of crucial commodities, that combination is back in the picture.

Spread expansion is bad news for leveraged strategies, and credit spreads are 10–15 basis points wider than their early-February lows.

“Spread expansion would be impacting levered strategies, eating into their yield and performance by a factor of equity plus leverage multiple,” Strano says. “A 15-basis-point expansion in spread with three times leverage strips 60 basis points from performance. We expect spreads to continue widening if the Middle East conflict continues to spread and oil shipments are impacted for a prolonged period.”

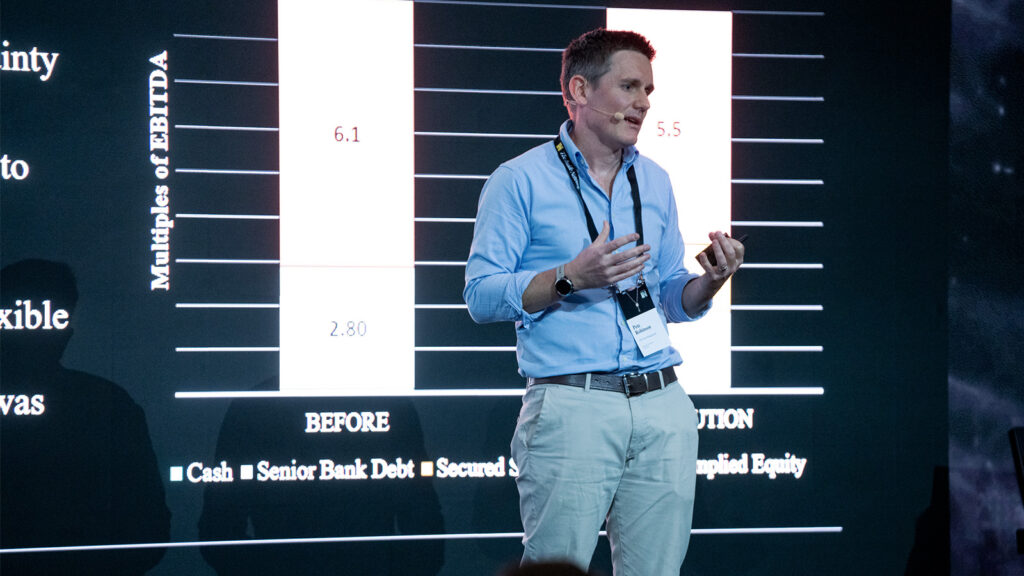

The unwelcome spectacle of an oil shock is hitting a market that was already, in some areas at least, “uncomfortably close to pre‑GFC behaviours,” where synthetic and physical leverage was more commonplace, says Strano. Toward the end of 2025, he says, the use of leverage was mainly occurring through the use of repurchase agreements (repo) of eligible collateral “up to an eye-watering 15-times for AAA-rated securities,” as well as through placement of senior secured leverage to enhance portfolio yields in both private and public credit portfolios.

New levered investment products that had recently entered the market were offering a floating-rate running yield from a portfolio likely comprised of major bank T2 hybrids (T2s) and investment-grade (IG) corporate bonds. Products such as these typically seek to enhance yield by deploying three to three-and-a-half-times leverage.

The investor thinks they have an underlying low-risk IG credit portfolio that can support the leverage. But working off an estimated credit-spread duration of about five years, a widening spread environment could “quickly overwhelm” underlying yields, says Strano. Spread expansion of about 100 basis points on a credit portfolio with three times leverage would generate a negative total return in the range of 10 per cent–15 per cent – in other words, equity-like drawdown risk from what is considered an underlying low-risk IG portfolio.

Given that fixed-income investors generally have a low tolerance for negative returns over a 12-month period, that is not what they expect, to put it mildly. But when market turbulence is pushing spreads wider, the use of leverage looks even more dubious. “We think that levered credit is incredibly poor compensation at current levels,” says Strano.

Indeed, Yarra Capital Management was concerned about the rise of leverage well before the missiles started flying on the weekend of February 28–March 1.

Writing in mid-February, Strano said: “At current spread levels, the probability of a plus or minus 100-basis-point move is weighted to the positive and in the current macroeconomic environment is entirely possible over the near to medium term. In such an event, which can occur two to three times each decade, the prospect of equity-like drawdowns from levered credit funds should give credit investors pause for thought.

“Put more simply, credit investors in these levered structures should be thinking hard about whether they are comfortable taking what is effectively equity drawdown risk for a miserly 1 per cent–2 per cent in additional yield. We would suggest that this represents incredibly poor compensation for the risk assumed at this point in the cycle.”

With spreads widening as markets deal with high levels of uncertainty, this thesis “very much still holds,” says Strano. “Risk-off events come in many forms and often result in valuation losses across risk assets.”

Sentiment is firmly in the grip of uncertainty over the duration of the Middle East war and the impact on oil supply/pricing, he says, but the broader thematic around underlying growth stimulus – that is, AI-related capital spending and government expansion (aged care, childcare, NDIS, defence and energy transition) – remains supportive for growth and commodity prices. “

Yields are likely to stay at a higher level which is supportive for fixed income, and credit more generally, with yields remaining attractive which should limit drawdowns for unlevered investment-grade funds,” says Strano. “There’s no question that the market is becoming more sensitive to the growing prospect of drawdowns and the illiquidity of private credit, and the probability of a plus- or minus-100-basis-point spread move remains skewed to the upside.’

Such a widening would affect levered and unlevered funds very differently. “In contrast to levered credit funds, both the Yarra Enhanced and Higher Income Funds are still providing attractive 6 per cent–7 per cent yields with precisely zero leverage, he says. “While it is true that a 100 basis-points widening in credit spreads would lead to value diminution for both these funds, high unlevered yields combined with active management should protect against negative returns over any 12-month period. We do not believe the same can be said of levered credit funds running a similar mix of underlying credit assets.”

James is an experienced senior journalist and editor of The Inside Network's publications.