Wednesday 4th October 2023

Banks lead Aussie market lower

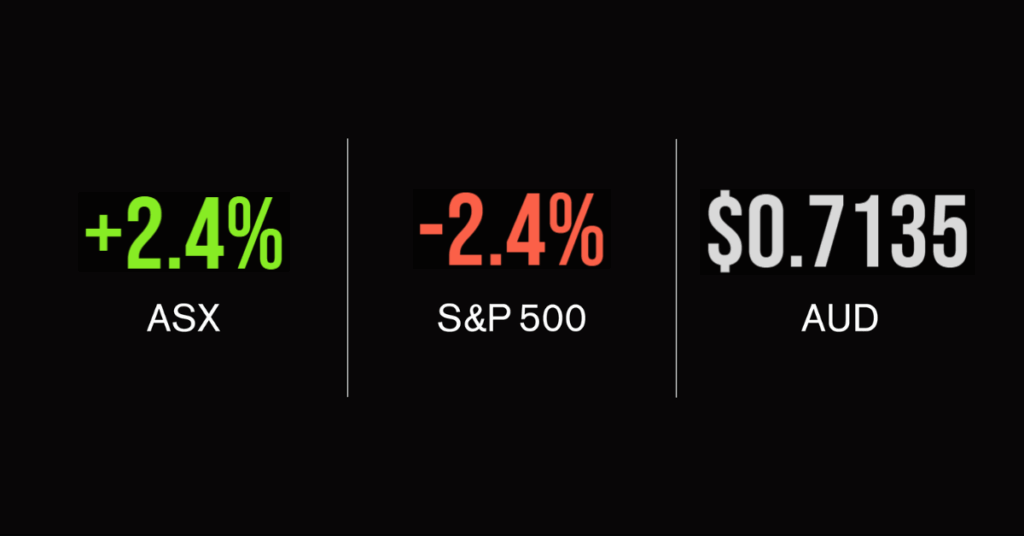

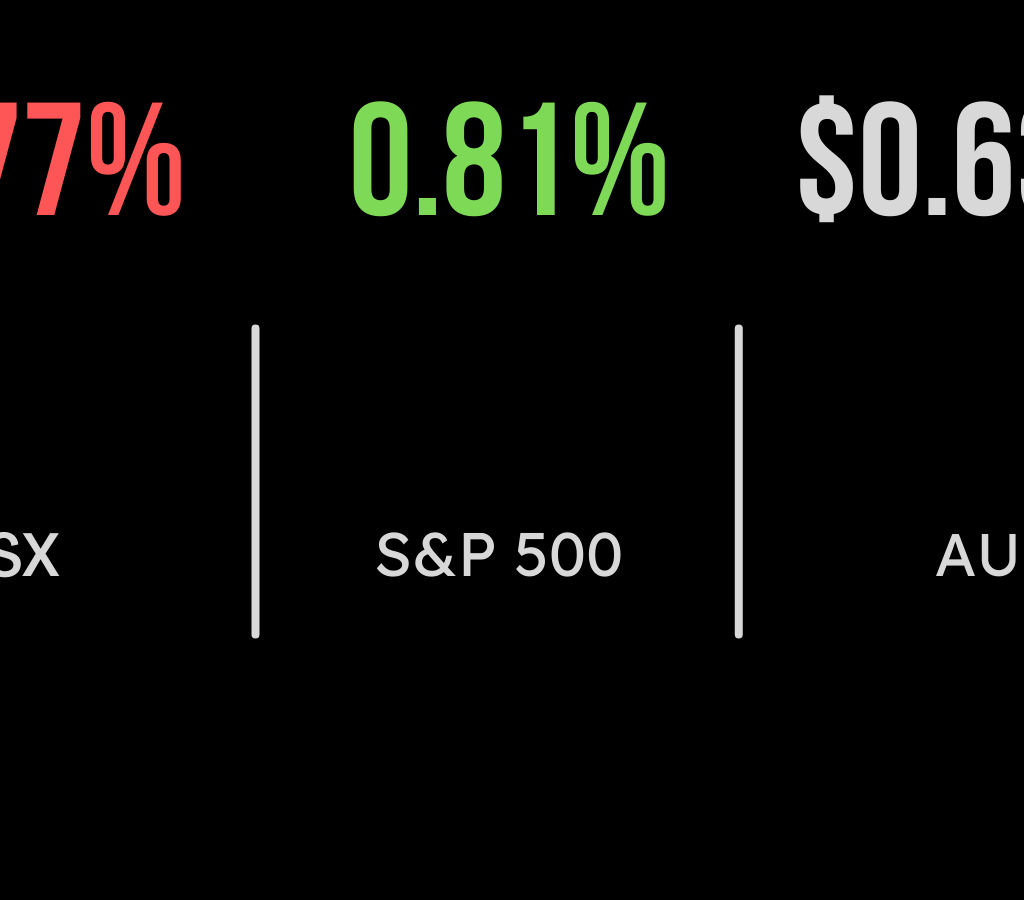

The Australian sharemarket closed at its lowest point in 11 months on Wednesday, hampered by a weak lead-in from Wall Street, and its interest-rate worries. The benchmark S&P/ASX 200 ended the session down 53.2 points, or 0.8 per cent, to 6890, its lowest close since November 3. Banks had a bad day, with the financials sub-index down 1.5 per cent, the worst performer of the S&P/ASX 200’s 11 industry groups. ANZ dropped 49 cents, or 1.9 per cent, to $24.92; National Australia Bank slid 48 cents, or 1.7 per cent, to $28.31; Commonwealth Bank dipped $1.60, or 1.6 per cent, to $98.09; and Westpac closed 31 cents, 1.5 per cent, weaker at $20.74.

Afterpay’s owner Block Inc. sank a further $1.65, or 2.4 per cent, to $66.11 after analysts at Citi cut their price target for the payments stock from $90 to $65. Block shares, which are dual-listed on the ASX and New York Stock Exchange, have almost halved in value in the past two months, and Block’s total market capitalisation has fallen to $US25.56 billion ($40.5 billion) – meaning that it is now worth less than what Block paid for Afterpay in 2021.

On the industrial front, Telstra was down 5 cents, or 1.3 per cent, to $3.78; Qantas shed 9 cents, or 1.8 per cent, to $4.93; Ansell lost 26 cents, or 1.2 per cent, to $21.51; and software player Data#3 surged 22 cents, or 3.3 per cent, to $7.00.

Resources mostly lower

In big mining, BHP eased 12 cents, or 0.3 per cent, to $43.72; but Rio Tinto advanced 82 cents, or 0.7 per cent, to $113.62; and Fortescue Metals gained 5 cents, or 0.2 per cent, to $20.78. On planet lithium, producer Allkem gave up 25 cents, or 2.2 per cent, to $10.90; fellow producer Pilbara Minerals weakened 4 cents, or 1 per cent, to $4.05; IGO, which mines nickel as well as lithium, fell 32 cents, or 2.6 per cent, to $12.05; and Mineral Resources slipped 82 cents, or 1.3 per cent to $63.33, after finalising a $US1.1 billion debt offer. Among the lithium project developers, Core Lithium lost 2.5 cents, or 6 per cent, to 39.5 cents; US-based Piedmont Lithium eased 1.5 cents, or 2.5 per cent, to 58.5 cents; and Lake Resources softened 1 cent, or 5.7 per cent, to 16.5 cents; but Liontown Resources, where iron ore magnate Gina Rinehart appears close to being able to block the $6.6 billion takeover offer by the world’s biggest producer of the battery metal, Albemarle, picked up 2 cents, or 0.7 per cent, to $2.97. Rinehart has bought 14.7 per cent of Liontown. In coal, the sector was led downward by Coronado Global Resources, which dropped 9 cents, or 5.1 per cent, to $1.685; while Whitehaven Coal mislaid 9 cents, or 1.3 per cent, to $6.84; New Hope Corporation retreated 11 cents, or 1.7 per cent, to $6.23; Stanmore Resources was down 6 cents, or 1.6 per cent, to $3.60; and Yancoal Australia gave up 13 cents, or 2.5 per cent, to $5.10.

In gold, Ramelius Resources closed 6 cents, or 4.3 per cent, higher at $1.465; Gold Road Resources added 3 cents, or 1.9 per cent, to $1.605; Evolution Mining strengthened 5 cents, or 1.6 per cent, to $3.17; Capricorn Metals gained 9 cents, or 2.3 per cent, to $4.02; and Northern Star advanced 14 cents, or 1.4 per cent, to $10.18; but West African Resources eased 3 cents, or 4.2 per cent, to 69 cents. Copper producer Sandfire Resources lost 8 cents, or 1.3 per cent, to $6.02; and rare earths producer Lynas Rare Earths walked back 4 cents, or 0.6 per cent, to $6.50.

Unofficial jobs report surprises Wall Street In the US, stocks snapped a three-day losing streak as bond yields eased from 16-year highs. following the release of much weaker-than-expected jobs data. Economists had expected the ADP Non-farm employment report to show a gain of 160,000 jobs in September – in keeping with the gauge’s recent form of 150,000-plus gains – but the number came in at just 89,000 jobs. Although this is a private report (ADP Is a payroll processing firm) and the official jobs report does not come out until Friday), markets were surprised by the soft figure, and the tentative signs of a weakening jobs market. For the official jobs report, the economists’ consensus estimates that non-farm payrolls increased by 170,000 in September, down from a 187,000 increase in August, according to Dow Jones. But the pencil may be taken to those estimates between now and Friday.

The 30-stock Dow Jones Industrial Average gained 127.17 points, or 0.4 per cent, to close at 33,129.55. The broader S&P 500 index rose 34.3 points, or 0.8 per cent, to 4,263.75, and the tech-laden Nasdaq Composite index kicked up 176.54 points, or 1.4 per cent, to 13,236.01.

The yield on the US 10-year Treasury had risen as high as 4.884 per cent before the ADP jobs figure came out, but ended the day down 6.8 basis points, at 4.736 per cent. The 2-year yield slid 11.3 basis points, to 5.071 per cent. Gold traded US$2.38 lower, to US$1,821.30 an ounce, while the global benchmark Brent crude oil grade plunged US$4.93, or 5.4 per cent, to US$85.99 a barrel, and West Texas Intermediate crude slid US$5.01, or 5.6 per cent, to US$84.22 a barrel.

The Australian dollar is buying 63.21 US cents this morning, up from 63.05 US cents at the ASX close on Wednesday.

James is an experienced senior journalist and editor of The Inside Network's publications.