Wednesday 30th July 2025

The case for short-duration fixed income; three reasons to consider owning the short end of the curve

Short-duration fixed income offers attractive long-term, risk-adjusted returns with less volatility compared to well-known fixed income benchmarks, say Joanne Driscoll, Head of Short-Term Liquid Markets at Franklin Templeton Fixed Income.

The short end of the fixed income curve includes investments such as US corporate and government bonds, money market instruments, commercial paper, mortgage and asset-backed securities, agency securities and certificates of deposit We believe the short-duration part of the fixed income market is positioned to perform well in various interest-rate scenarios, providing greater return consistency and serving as a ballast against interest-rate volatility. And there are three main reasons for that.

From January 1978 through June 2025, as seen in the first chart, short-duration (one to three years) fixed income has delivered similar long-term annualised returns to well-known fixed income benchmarks, but with substantially less volatility (standard deviation), resulting in higher long-term, risk-adjusted returns (Sharpe Ratio).

We believe this makes it an appealing option for investors seeking stability and consistent performance over time. As a result, we find investors may want to consider incorporating short duration as a structural allocation into a diversified fixed income portfolio. Furthermore, we believe the lower volatility associated with short-duration fixed income can help reduce the overall risk of the portfolio, making it a prudent choice for risk-averse investors.

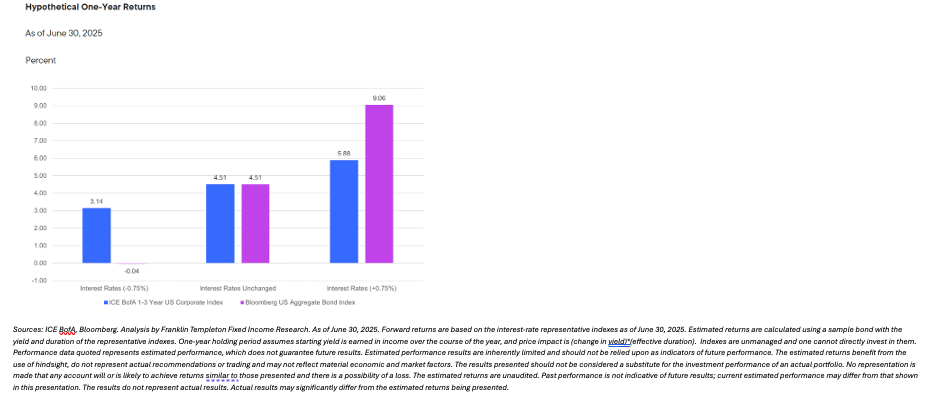

Reason #2: Short duration is set up to potentially perform well in various interest-rate scenarios

This chart illustrates three hypothetical interest-rate scenarios: one, interest rates move lower by 0.75 per cent; two, interest rates remain unchanged; and three, interest rates move higher by 0.75 per cent. With attractive yields and less interest-rate sensitivity, short duration is positioned to deliver greater return consistency versus core fixed income under these different interest-rate scenarios. Consequently, we believe owning short-duration fixed income can provide an attractive risk/return trade-off for investors who remain uncertain about the direction of US Federal Reserve policy, inflation impacts as a result of tariff negotiations, and fiscal dynamics in the United States. Overall, we believe short-duration fixed income is an attractive option for investors looking to mitigate the interest-rate volatility in their portfolios.

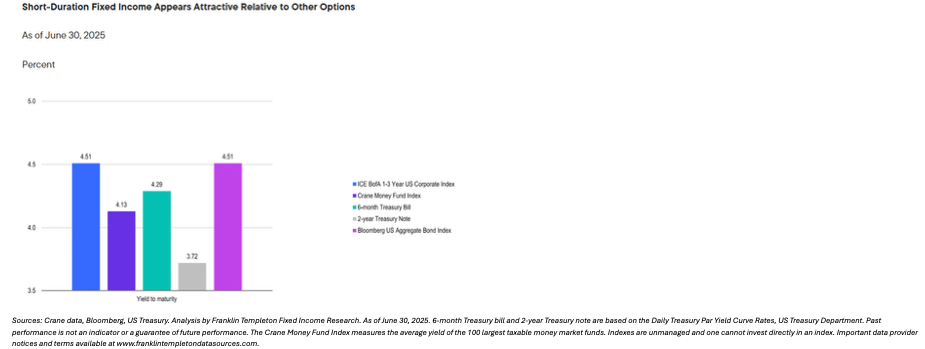

Reason #3: Short-duration yields appear attractive relative to cash-like options and core fixed income

Investors can capture higher yields in short-duration relative to “cash”-like investments, such as money market funds and short-term Treasuries, as seen in this chart below. We believe this yield advantage may continue to increase moving forward due to Fed policy, changing yield curve dynamics and reform-driven impacts on money market funds. We believe this makes short duration a compelling choice for investors looking to maximise returns while maintaining a focus on capital preservation and liquidity. Furthermore, short duration offers yields in-line with longer-duration fixed income that are inherently more volatile.

It should be stressed that the estimated returns benefit from the use of hindsight, do not represent actual recommendations or trading and may not reflect material economic and market factors. The results presented should not be considered a substitute for the investment performance of an actual portfolio. No representation is made that any account will or is likely to achieve returns similar to those presented and there is a possibility of a loss. The estimated returns are unaudited. Past performance is not indicative of future results; current estimated performance may differ from that shown in this presentation. The results do not represent actual results. Actual results may significantly differ from the estimated returns being presented.