Wednesday 26th April 2023

Central banks face a no-win situation: Ruffer

They can either tighten policy to squash inflation or ease to prevent financial contagion, but there's no right answer for central banks according to Ruffer's Duncan MacInnes.

When Bob Dylan released his seminal album Blood on the Tracks in January 1975, the US economy was in recession and suffering 12% inflation. The inflation appeared transitory and fell below 5% in 1976. Alas, the political and macroeconomic die had been cast for another inflationary spasm as recovery took hold. This time, it lasted the rest of the decade, peaking at over 15%. Does that sound familiar?

Today’s policymakers face a no-win situation. There will be blood on the tracks once more. Yet again, what the real economy needs, financial markets can’t handle.

Central bankers have competing goals: on the one hand, to forestall banking crises and contain financial contagion; on the other, to bring inflation down to target. The first requires monetary policy easing, the second monetary policy tightening.

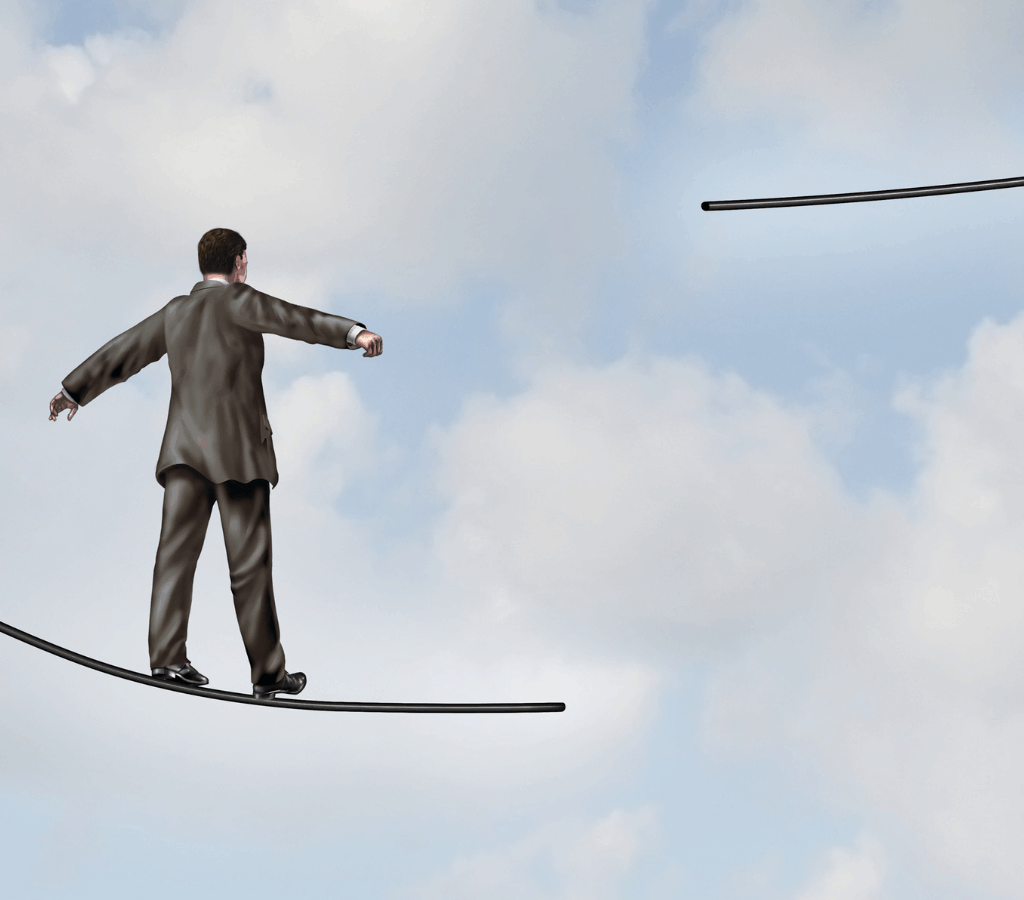

Like the man in this month’s image, policymakers face an impossible but unavoidable choice – let inflation gather steam, or act and risk a financial system calamity. There is no third way.

Of course, it’s central bankers’ job to project confidence. Here’s European Central Bank President Christine Lagarde on 22 March: “There is no trade-off between price stability and financial stability. We have plenty of tools to provide liquidity support to the financial system if needed and to preserve the smooth transmission of monetary policy.

In fact, there is always a trade-off between monetary stability and financial stability – but that trade-off is particularly acute when inflation is in the high single digits and financial institutions are disappearing at weekends.

Central bankers have convinced themselves they can take a targeted ‘macro-prudential’ approach. They believe their inflation and financial stability objectives are distinct, and addressable with different tools. Rate hikes to fight inflation. And liquidity provisions to preserve banking stability. But sooner or later all these support packages begin to look like QE.

Since May 2022, the US banking system has lost $700 billion of deposits – a large portion of which followed the dramatic implosion of Silicon Valley Bank last month.1 The money multiplier means the true impact is greater. Investors now worry about the return of their investment rather than the return on their investment.

This mini-banking crisis has caused a sudden tightening in credit availability and lending criteria. This will hit the real economy. Regional banks are the primary source of credit for small and medium-sized businesses and commercial real estate.

To offset this tightening, the Fed has sluiced the system with ‘temporary’ liquidity, unwinding more than half of last year’s quantitative tightening. They did this with a new acronym called the BTFP (bank term funding program). One observer suggested this stands for “buy the flipping pivot!” Unless we misheard.

The apparent free will of central bankers is proving illusory. Ultimately, their primary goal of controlling inflation takes a back seat when it begins to threaten the stability of the financial system. Higher inflation is the least painful option when the alternatives, in extremis, could echo the 2008 financial crisis or the even Great Depression. But first the man on the street needs to feel enough pain to beg for the mercy of the monetary firehose. We are getting closer to that point. Time to seek shelter from the storm.