Sunday 24th July 2022

Stocks deliver best week since March, tech surge continues, Magellan boost

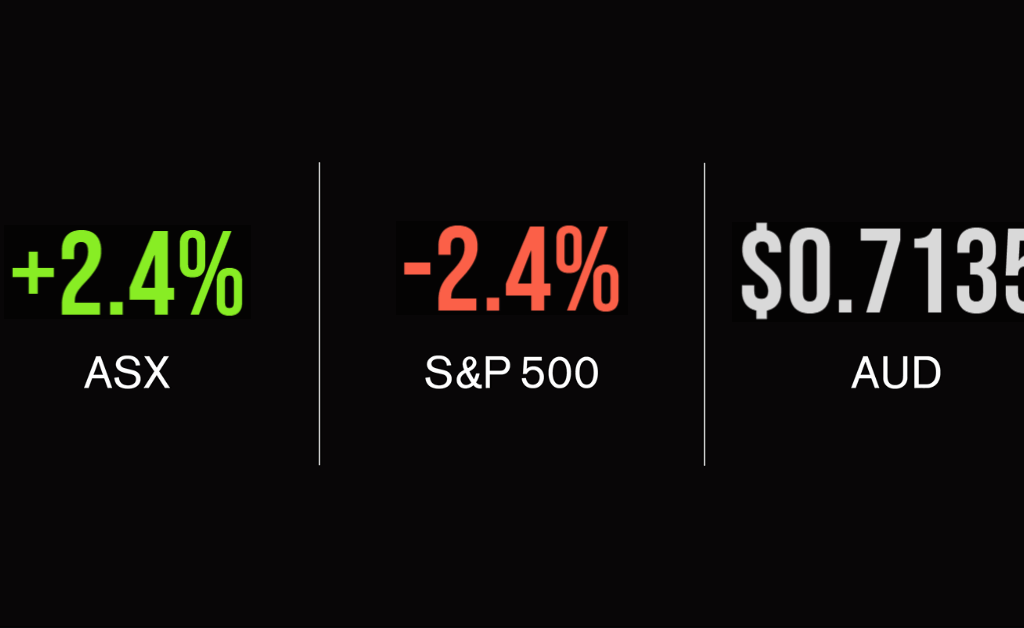

The S&P/ASX200 delivered the best week since March this year gaining 2.8 per cent despite weakening slightly on Friday.

The driver has been a turnaround in the outlook for interest rates and signs of a slowing economy, with the tech sector up 7.1 per cent for the five days.

On Friday it was all about the financials and real estate sectors, which gained 0.9 and 0.6 per cent respectively, benefitting from more positive earnings news in the US.

Magellan (ASX: MFG) was a key contributor gaining 2.3 per cent after showing signs of strong fund performance once again; the stock gained 20 per cent for the week.

Smaller technology companies Pointsbet (ASX: PBH) and Zip (ASX: ZIP) added 16 and 13 per cent each, but remain well below their prior highs.

Insurance Australia Group (ASX: IAG) was a rare detractor, falling 4.1 per cent over the five days after warning of weaker profits on the back of a spike in claims.

Domino’s (ASX: DMP) was also sold off after the US-equivalent reported inflation and cost challenges.

Over the week, financials drove the market, with the Commonwealth Bank (ASX: CBA) and National Australia Bank (ASX: NAB) adding 3.7 and 4.1 per cent on hopes that rate hikes were set to slow.

But Zip and Brainchip were the standouts up 54 and 36 per cent in just five days, followed by fund manager Pendal (ASX: PDL) which added 26 per cent after confirming further takeover talks.

US markets falls into close, Snap Chat tanks, economic data weakens

US markets paused on Friday after a relatively strong week with a shocking report from social media app Snap Inc. (NYSE: SNAP) sending the technology sector down heavily ahead of a massive week of reporting.

Shares in Snap fell by 39 per cent in a single session after the company reported a more than doubling of it’s quarterly loss to US$422 million on sales growth of just 13 per cent.

The concern was really about a fall in advertising sales, with the likes of Alphabet (NYSE: GOOGLE) and Meta (NYSE: META) falling 5 and 7 per cent along with Snap.

The Nasdaq finished the day down 1.9, but gained 3.3 per cent for the week, the S&P500 down 1 but up 2.6 and the Dow Jones falling just 0.4 per cent and gaining 2 per cent for the week.

There are more signs of a weakening economy with the latest manufacturing PMI reading showing the biggest slowdown in activity since the pandemic, which comes ahead of a potential 75 basis point rate hike by the Federal Reserve.

Shares in Verizon (NYSE: VZ) also fell by more than 6 per cent citing greater competition as being behind a fall in margins and higher inflation impacted on customer spending.

Amazon expansion continues, finding neutral, short-term or long?

Further evidence to look overseas for growth was on show with Amazon’s (ASX: AMZN) latest announcement.

The group is buying healthcare provide One Medical, which offers subscription doctor and healthcare services for US$3.9 billion.

Amazon is seeking to expand their skillset into other key sectors of the economy that are ripe for disruption, something that is difficult to find in the more traditional Australian sharemarket.

News this week that Russia and Ukraine were set to sign a deal to release grain exports, but also that Russia may reopen exports of gas to Western Europe have been met with a degree of caution.

Many companies have benefited from a supply-driven jump in prices, but should these markets return to any state of normalcy those profits, and share prices may reverse and quickly.

Finally, it was all about the central banks, with the ECB hiking rates for the first time in 11 years.

In Australia, the RBA Board confirmed they are seeking to increase the cash rate to what they call the ‘neutral rate’ while also indicating they do not know what this rate may be.

That is, they may well increase interest rates until ‘something breaks’, but what level this remains unknown to most, putting economic growth at risk.

Drew is editor of The Inside Network's publications and a principal adviser at Wattle Partners.